Liquidity crunch intensifying

Liquidity crunch in the banking sector is deepening due to slow growth of deposits and a lethargic recovery of loans.

The majority of the banks are now offering 11-12 percent interest rate to attract deposits and yet they are floundering.

The rise in default loans, an erosion of public confidence in the banking sector and the latest central bank’s move to ease the loan classification rules are largely blamed for the ongoing liquidity crisis, analysts said.

The ongoing implementation of mega infrastructural projects is also fuelling the cash shortage as lenders have been providing import financing to materialise those by way of purchasing the dollar from the central bank, they said. A total of $2.14 billion was purchased by banks between July 1 last year and May 2 this year.

“We are offering 12.50 percent interest for one-year term deposit. Even then we are not getting cash,” said a managing director of a non-bank financial institution that relies mostly on banks for funds.

He does not know when the crisis would be resolved as banks have been in severe cash crunch for the past one year. His concern is evident in the banking sector also.

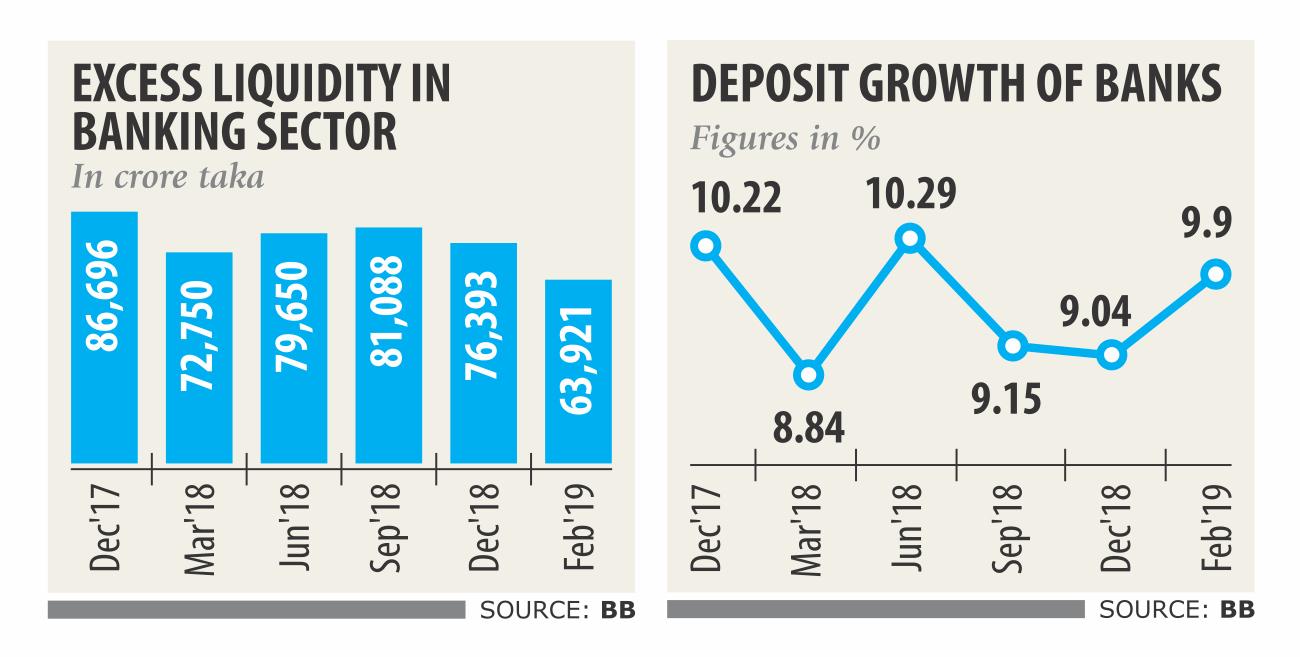

Banks enjoyed more than 10 percent deposit growth in 2017, but the situation took a turn for the worse last year, with growth hovering around the 8-9 percent mark.

The lower deposit growth also had an adverse impact on banks’ excess liquidity as the surplus amount stood at Tk 63,921 crore as of February, down 5.82 percent from a month earlier and 14.56 percent year-on-year, according to data from the central bank.

The upward trend of default loans stemming from financial scams and weak supervision by the central bank is eroding the confidence of customers in the banking sector, according to a paper of the Bangladesh Institute of Development Studies.

At the end of 2018, the total default loans in the banking sector stood at Tk 93,370 crore, which is 10.30 percent of the total outstanding loans.

Clients are now concerned about the fragile corporate governance in the banking sector, which is discouraging them to park their deposit with banks, said a managing director of a private bank, wishing not to be named.

The government had instructed its entities last year to keep deposits with banks at an interest rate of 6 percent, but they did not follow the order at all.

In April last year, sponsors of private banks had fixed the interest rate for deposits at 6 percent and for lending at 9 percent after bagging a set of facilities from both the central bank and the government.

The cash-strapped banks are now hunting deposit from the government organisations by offering more than 10 percent interest, which is also responsible for the distortion of the market, said the MD of the non-bank.

In many cases, banks are forced to offer illegal commission to the government officials to manage the deposit along with giving more than 10 percent interest, according to him.

The majority of banks have failed to get government deposit despite repeated attempts, said Shafiqul Alam, managing director of Jamuna Bank.

If they kept deposit with banks in a proper manner, the situation would have improved, he said.

The high rate on deposit has also pushed the interest rate on lending: banks are now disbursing loans at 13-16 percent interest.

Some banks are also luring in depositors from others, said MA Halim Chowdhury, managing director of Pubali Bank.

“My bank’s liquidity base is good enough, but we have recently been forced to increase the interest rate on deposit slightly as some clients have taken an attempt to withdraw their fund,” he said.

A large number of defaulters have recently stopped regularising their default loans, eyeing the upcoming relaxed rescheduling policy of the central bank, said Syed Mahbubur Rahman, chairman of the Association of Bankers, Bangladesh, a platform of the managing directors of private banks.

They are arguing that only 2 percent down payment of default loans will be given once the central bank’s policy comes into effect, he said.

In such a situation, cash recovery from defaulters has become even more difficult, said Rahman, also the managing director of Dhaka Bank.

The decline in deposit growth has also had a negative impact on the loan-deposit ratio as 20 banks failed to keep their regulatory ratio within the permissible limit in the first week of last month.

Loan-deposit ratio in private banks stood at 86.73 percent on April 5, up from 85.93 percent on December 31 last year, according to data from the Bangladesh Bank.

On January 30 last year, the central bank had set the June 2018 deadline to lower their loan-deposit ratio to 83.5 percent from 85 percent for conventional banks and to 89 percent from 90 percent for Shariah-based banks.

Seeing the failure of many lenders to bring down the ceiling, the central bank on March 7 extended the deadline to September.

The new loan classification policy, which calls for a six-month grace period, will hit banks’ liquidity base further, Rahman said.

He, however, expressed hope that clients might shy away from national savings certificates as banks continue to raise the interest rate on deposit products.